How Much Super Should You Have To Retire?

Retirement might seem like a far off dream for many in the workforce, but it’s never too early to start thinking about how much money you might require to live comfortably in your golden years.

Your super balance will most likely fund your retirement, so knowing how well it is performing at your current age is a critical way to address performance issues and optimise its path going forward. You want to make sure you’ll be getting the most out of your super so that when it comes to retiring, you can afford the lifestyle you want.

The amount of super that you may need to live comfortably during your retirement may depend on a range of factors, such as expenses that you may incur, outstanding debts you may have and whether you will be eligible for other types and forms of income (such as through investments, savings, an inheritance or the Age Pension).

How much super do I need for a 'comfortable retirement'?

A good place to start is with the end in mind. For those wanting a ‘comfortable retirement,’ the average super balance at retirement should be around $640,000 for couples and around $545,000 for singles.

According to figures set out in March 2021, those who are looking to retire today (regarding individuals and couples around the age of 65) would need an annual budget of around $44,412 or $62,828 to fund a comfortable lifestyle. For a modest lifestyle, they would need an annual budget of $28,254 or $40,829 respectively.

What’s the average super balance by age, and is it enough to track towards a ‘comfortable retirement’?

Everyone’s situation is different, and their super balance will likely reflect those differences.

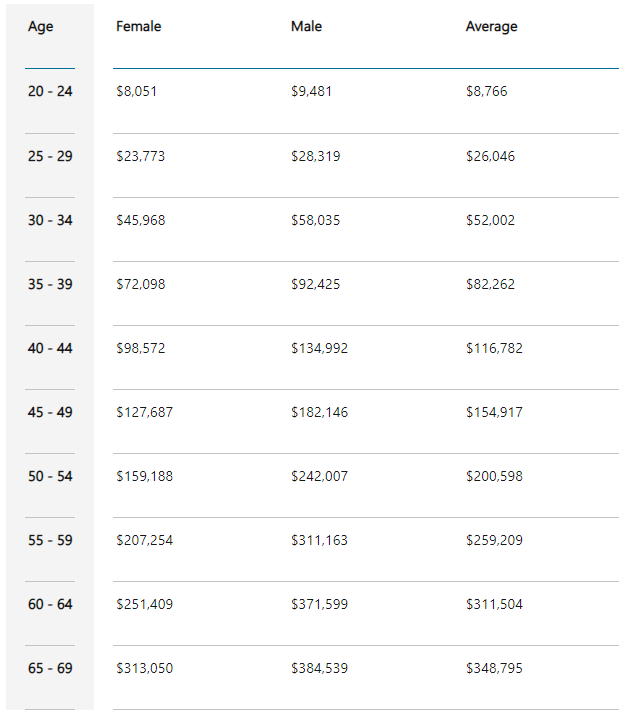

Men and women may have different super balances due to pay gaps, salary differences and potentially the amount of time they have actually spent working (maternity leave, working part-time versus full-time etc, taking time off work for travel, etc.). As an example, a woman in the 20-24 age bracket may have an average super balance of $8,051, while a man in the same bracket is expected to have an average balance of $9,481. In the 40-44 age bracket, the average super balance for men is $134,992, while women in that same age group may only possess $98,572.

The table below shows the average super balances of Australians across different age groups and genders.

Are these average balances enough to be tracking towards a ‘comfortable retirement’?

How much is ‘enough’ will change for every individual.

The table below suggests (that on average) there’s a potential shortfall in today’s super balances to be on track for a ‘comfortable retirement’, and shows where your super balance should be at your age today.

How to improve things?

So how can you make certain that your superannuation gets the boost it needs to fund your retirement? We can suggest the following:

Track down lost super to make sure that you’re not paying for multiple fees on different accounts.

Consider whether consolidating your funds might be a worthwhile option, to keep easier track of them.

Review your investment options (you may want to consider switching to a more growth-focused super investment option, for example).

Review your super at least once a year, and check the fund’s performance, fees that you are paying, what insurance you might have inside your super and if it is still suitable for your current needs.

If your cashflow allows it, salary sacrifice additional superannuation from your wages (if you are an employee).

If you are self-employed or run a business, contribute up to the maximum deductible superannuation contribution ($27,500 for the current financial year) because it is tax effective (15% tax in super versus much higher personal marginal tax rates).

If you come into money (e.g. from inheritance or sale of a property), consider making a non-concessional contribution (the maximum for the current financial year is $110,000) to boost your balance.

If you are looking to sell your business, consider contributing some of the sale proceeds into your super fund to significantly reduce the tax you would otherwise pay due to the capital gain made.

If you’re looking towards your future and want more advice on how to plan for your retirement with regard to your superannuation, you can speak with us or your super provider.

Disclaimer:

The information contained in this publication is for general information purposes only, professional advice should be obtained before acting on any information contained herein. The receiver of this document accepts that this publication may only be distributed for the purposes previously stipulated and agreed upon at subscription. Neither the publishers nor the distributors can accept any responsibility for loss occasioned to any person as a result of action taken or refrained from in consequence of the contents of this publication.